Capex Spending Will be the Moat

Hello everyone,

As many of us have noticed, CapEx spending has surged recently, particularly among mega-cap tech companies, with heavy investment flowing into data center.

Much of this spending has faced strong criticism online from prominent investors. I was also concerned about the potential rapid depreciation of some of these assets, but this new perspective may change your mind.

This wave of investment isn’t limited to data centers. It’s extending into other critical infrastructure areas, especially subsea cables and related connectivity buildouts.

The thesis is…

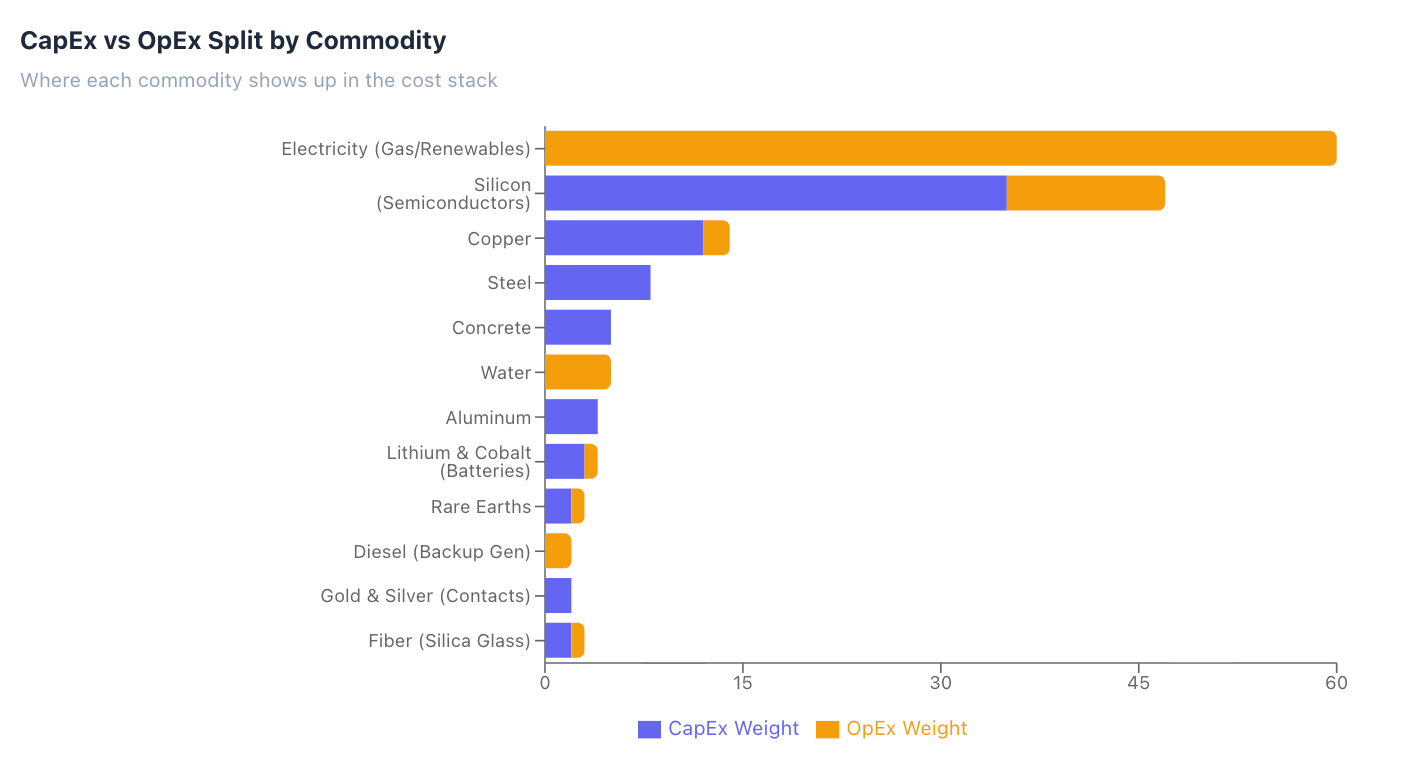

Rising commodity prices and elevated interest rates are escalating the required rate of returns and the cost of building new physical infrastructure across semiconductors, telecoms, utilities and even subsea cables. This creates a self-reinforcing barrier to entry that protects incumbent asset-heavy companies. The 2025 metals run-up and now the 2026 energy shock (Brent $65 to $100+/bbl) has accelerated this dynamic, with optical fiber prices up +336%, copper +36% and subsea cable project costs up +39.5%.

As software becomes increasingly commoditised by sharp gains in AI-driven productivity, barriers to entry are shifting toward infrastructure. In response, many mega-cap technology companies have been investing heavily in infrastructure.

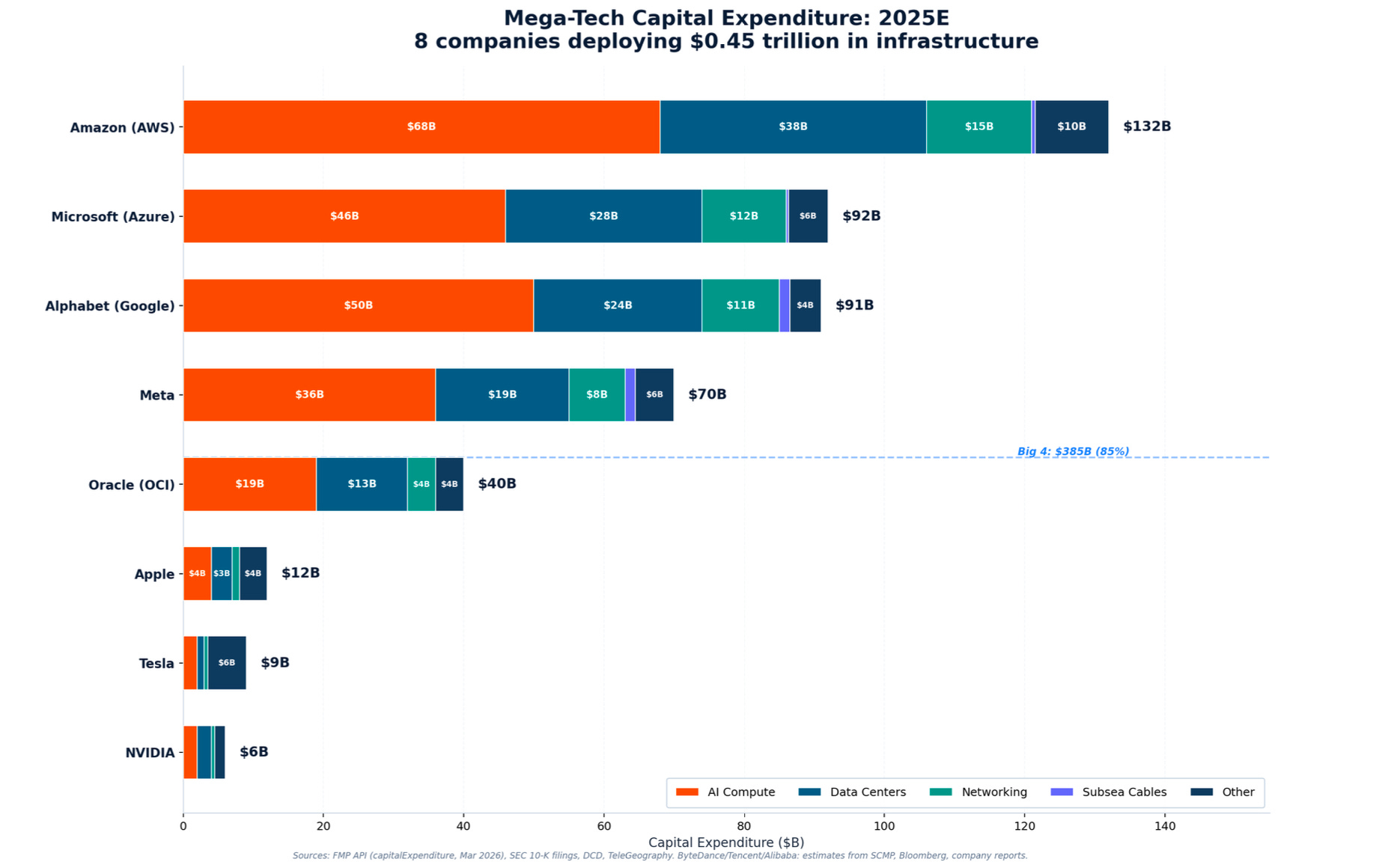

The largest tech firms are now deploying unprecedented levels of capital expenditure, driven primarily by AI infrastructure such as data centers, GPU clusters, custom silicon and continued cloud expansion. In 2025, the Mag 7 + Oracle spent a combined $450 Billlion in CapEx.

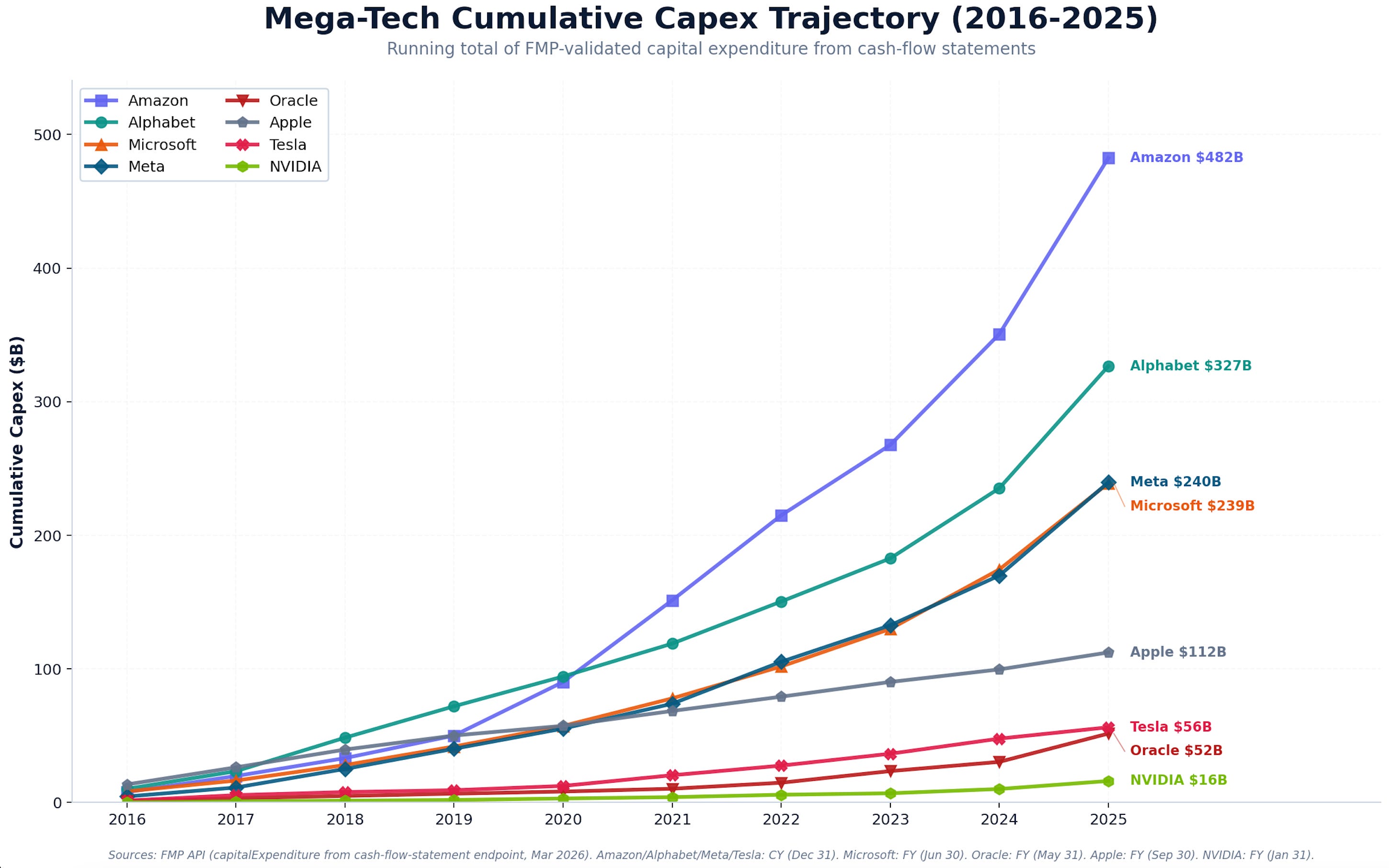

To put this into perspective, the combined CapEx of these eight companies over the past decade (2016 to 2025) totals roughly 1.52 trillion dollars, with nearly one third of that spent in just the last two years during the AI surge.

An angle I rarely see discussed is the relative value of these assets. In my opinion the value has increased materially, driven by rising costs in metals, energy and labor. Any company attempting to compete with these capital-intensive businesses by building their own infrastructure today must do so in a structurally higher-cost environment, facing weaker unit economics and competing against incumbents that built their capacity before this surge in input prices.

Lets take a look at an AI datacenter as an example..

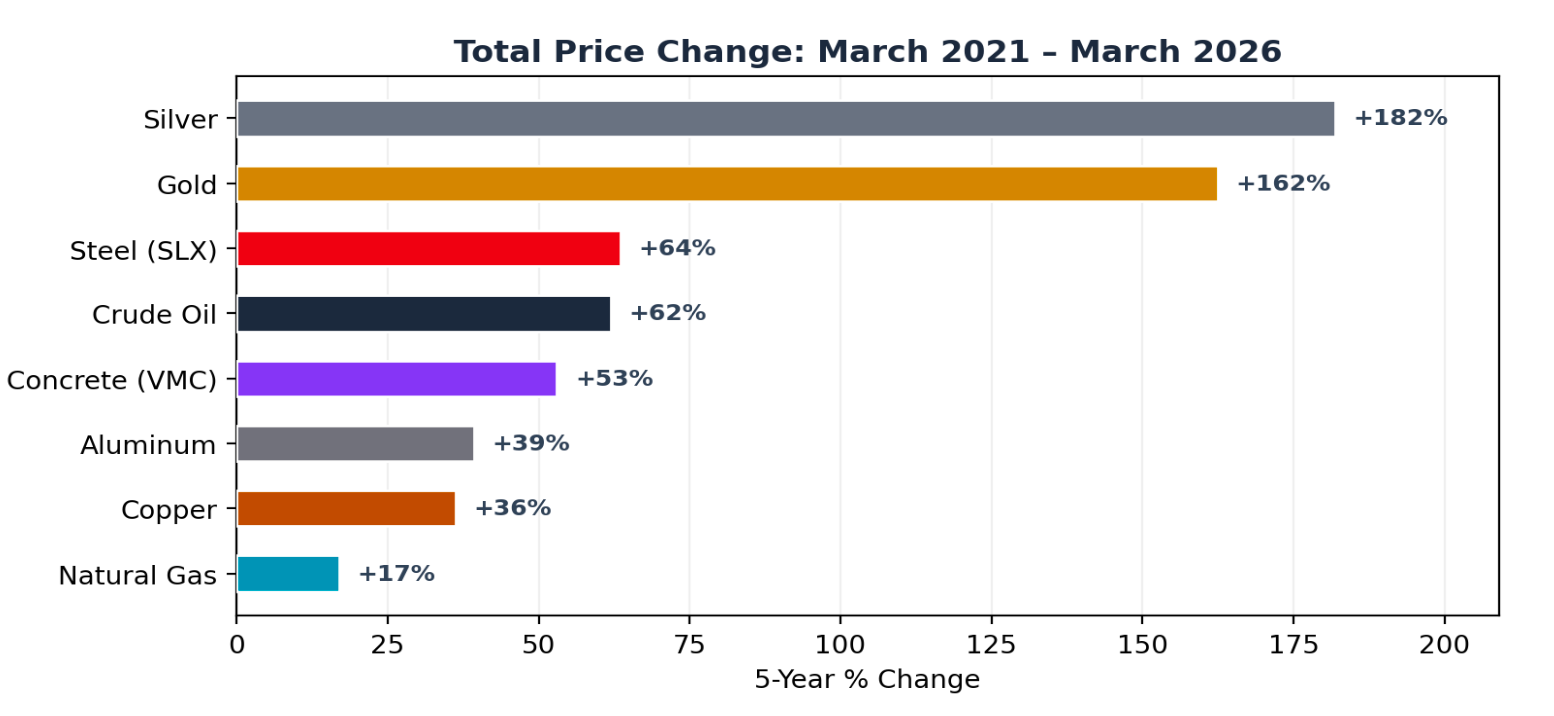

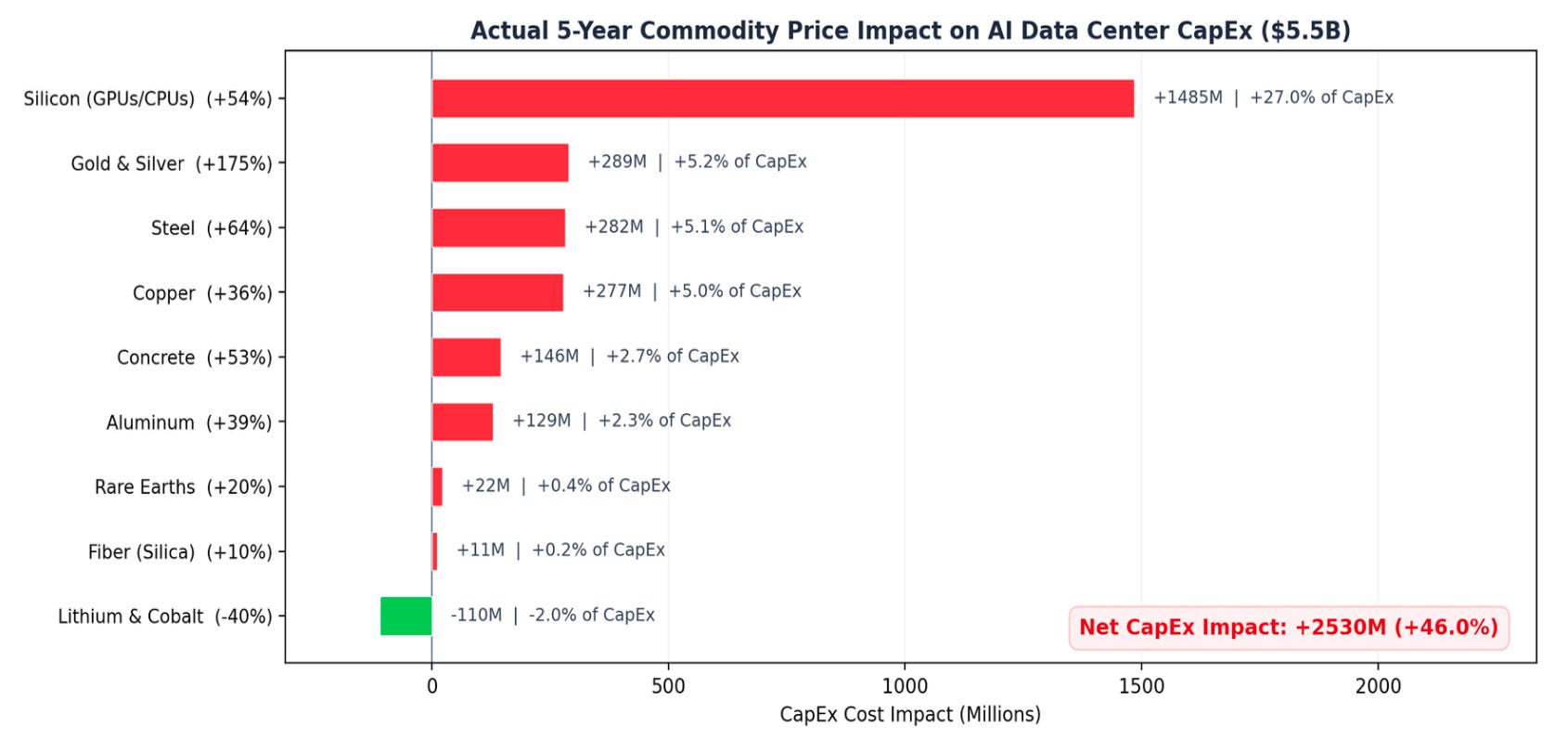

Most of the commodities used in AI datacenter CapEx, such as silicon, copper, steel, concrete and aluminium, have seen significant price appreciation over the past five years. With gold and silver surging by over 162% and 182%, respectively.

As a result of these price increases, pricing power in these businesses is likely to strengthen over time, though it may not immediately translate into higher profits from a strategic standpoint. Keeping margins compressed can be intentional, as it pressures competitors and makes entry economically unattractive.

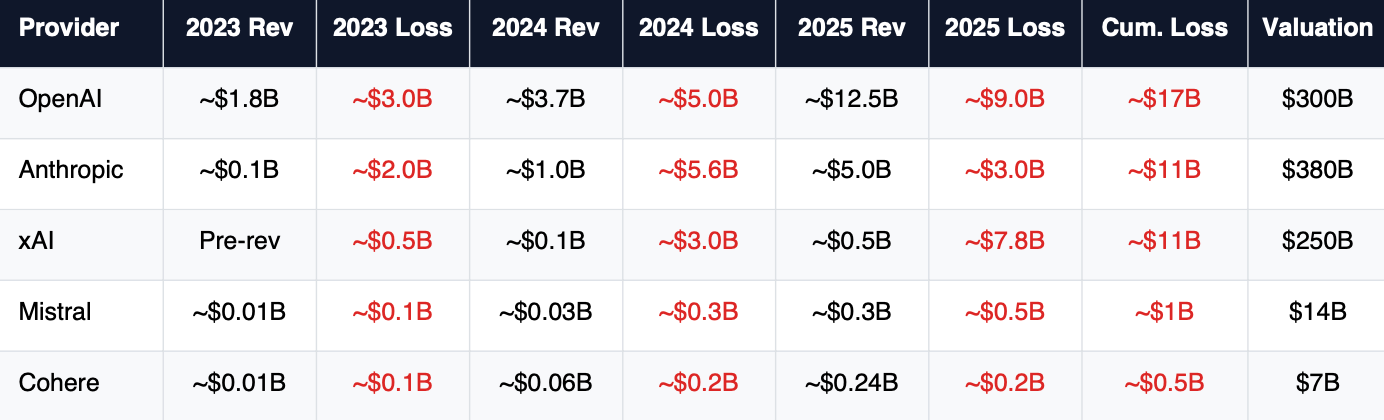

The mounting losses in the LLM space not only protect market share from competitors but also raise the cost and complexity of building rival data centers, reinforcing the dominance of established players.

For non-US tech players, competing at this scale of CapEx is extremely difficult. It would likely require substantial government support, and even then, success would depend on securing long-term demand for their cloud services. In contrast, US incumbents provide not only infrastructure but also the software stack, reinforcing their competitive and ecosystem advantage.

As a simple illustration, a $5.5 billion datacenter project five years ago would now require an additional $2.5 billion in CapEx, an increase of roughly 46% over the original investment.

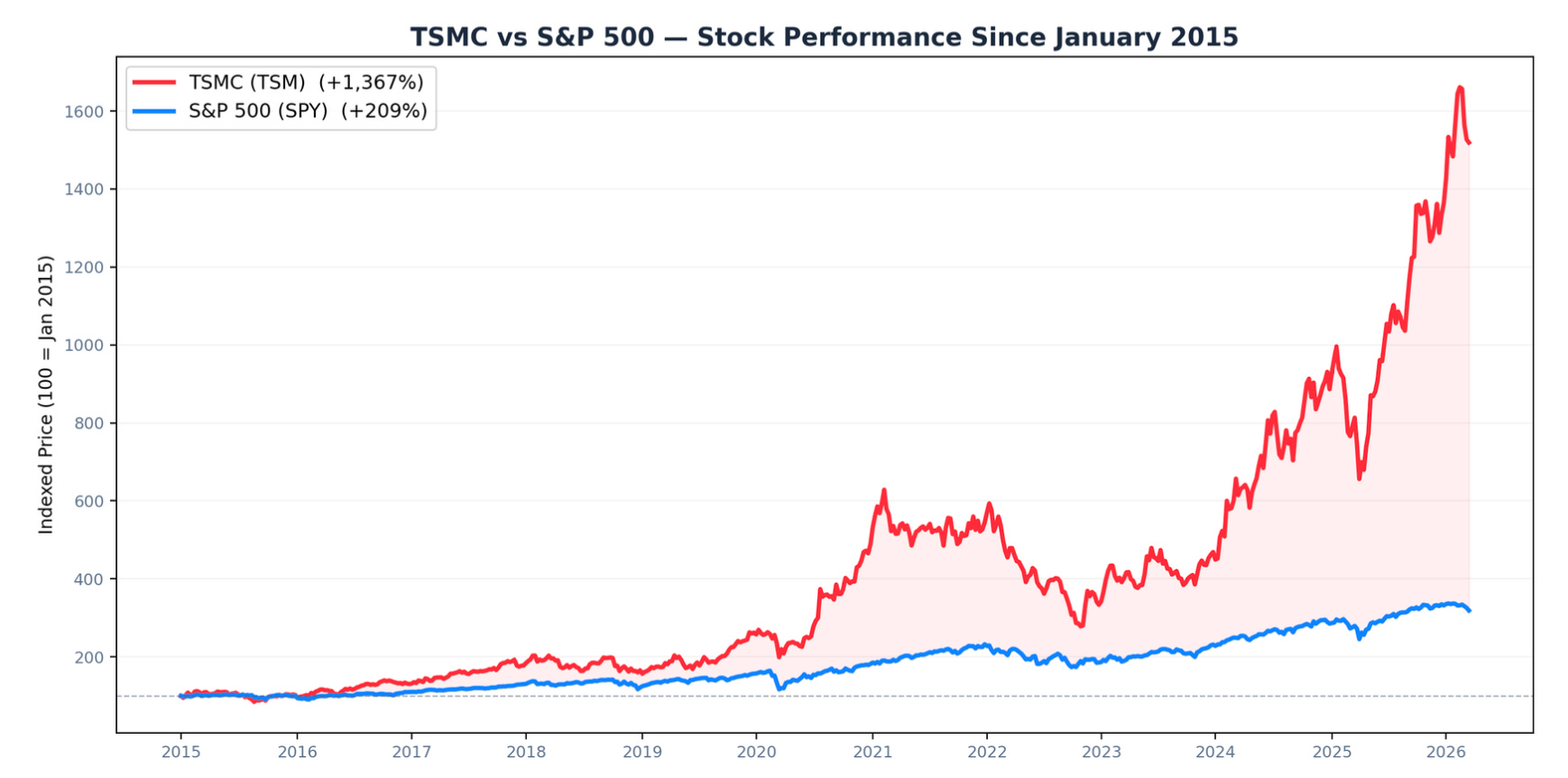

There are clear examples where these dynamic had already played out. Taiwan Semiconductor TSM 0.00%↑ is a good example. Fab construction costs have risen from $5B to $20B+ per facility which allows for TSM to run at significantly higher margins than competitors.

The same dynamic observed in semiconductors is increasingly evident across AI infrastructure, particularly in data centers and subsea cable networks. As input costs rise across labor, energy, materials and specialised equipment, the economics of building large-scale infrastructure have shifted materially.

Companies like Amazon AMZN 0.00%↑, Microsoft MSFT 0.00%↑, and Google GOOGL 0.00%↑ were able to deploy massive capital into data centers before this recent inflationary wave, securing access to power, land and hardware at significantly lower costs. Today, new entrants face a much higher cost base and tighter constraints, particularly around energy availability and high-performance compute.

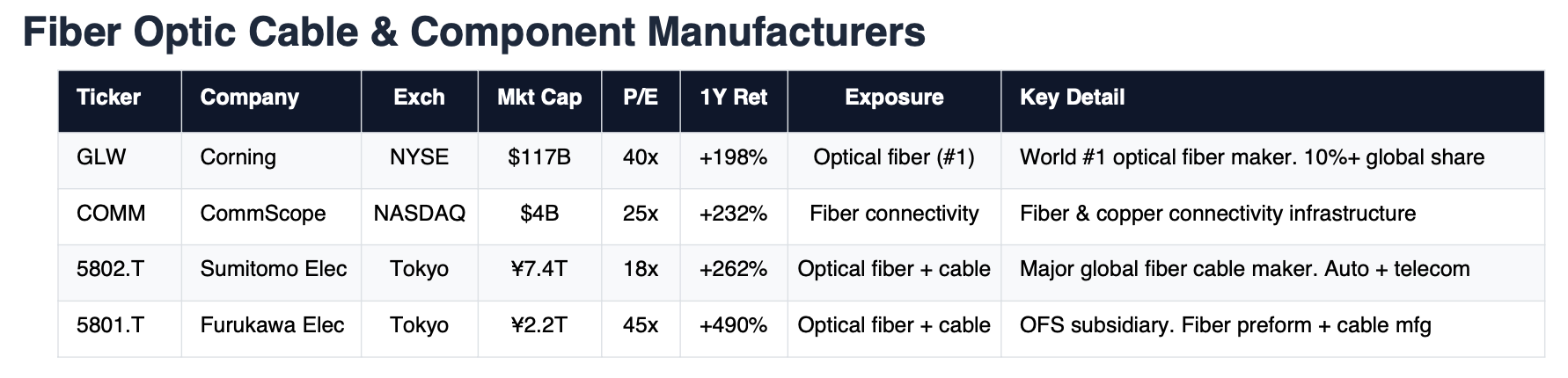

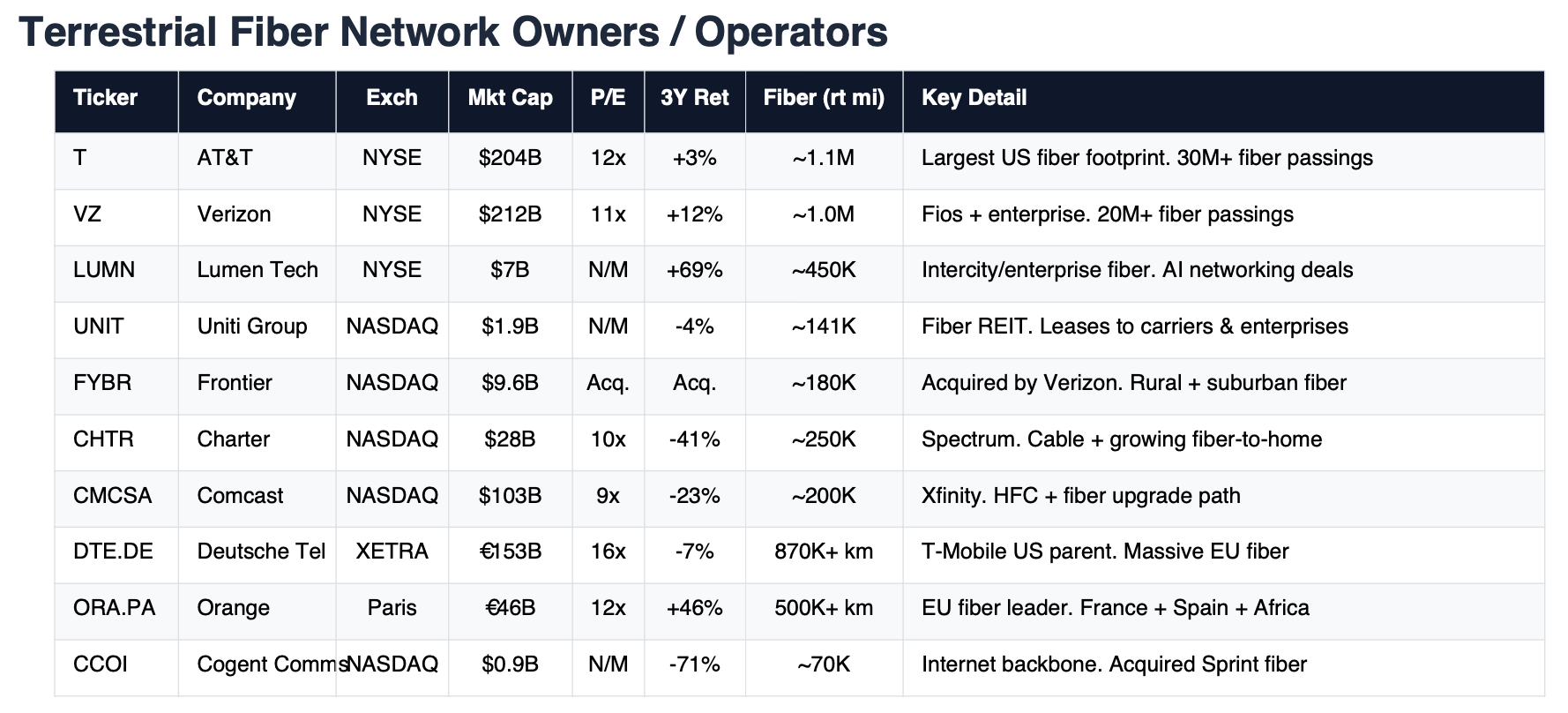

A similar pattern is unfolding in global connectivity infrastructure. Subsea cables, which form the backbone of international data transfer, are highly capital-intensive and have also become more expensive to deploy due to rising costs in raw materials, marine engineering and specialized labor.

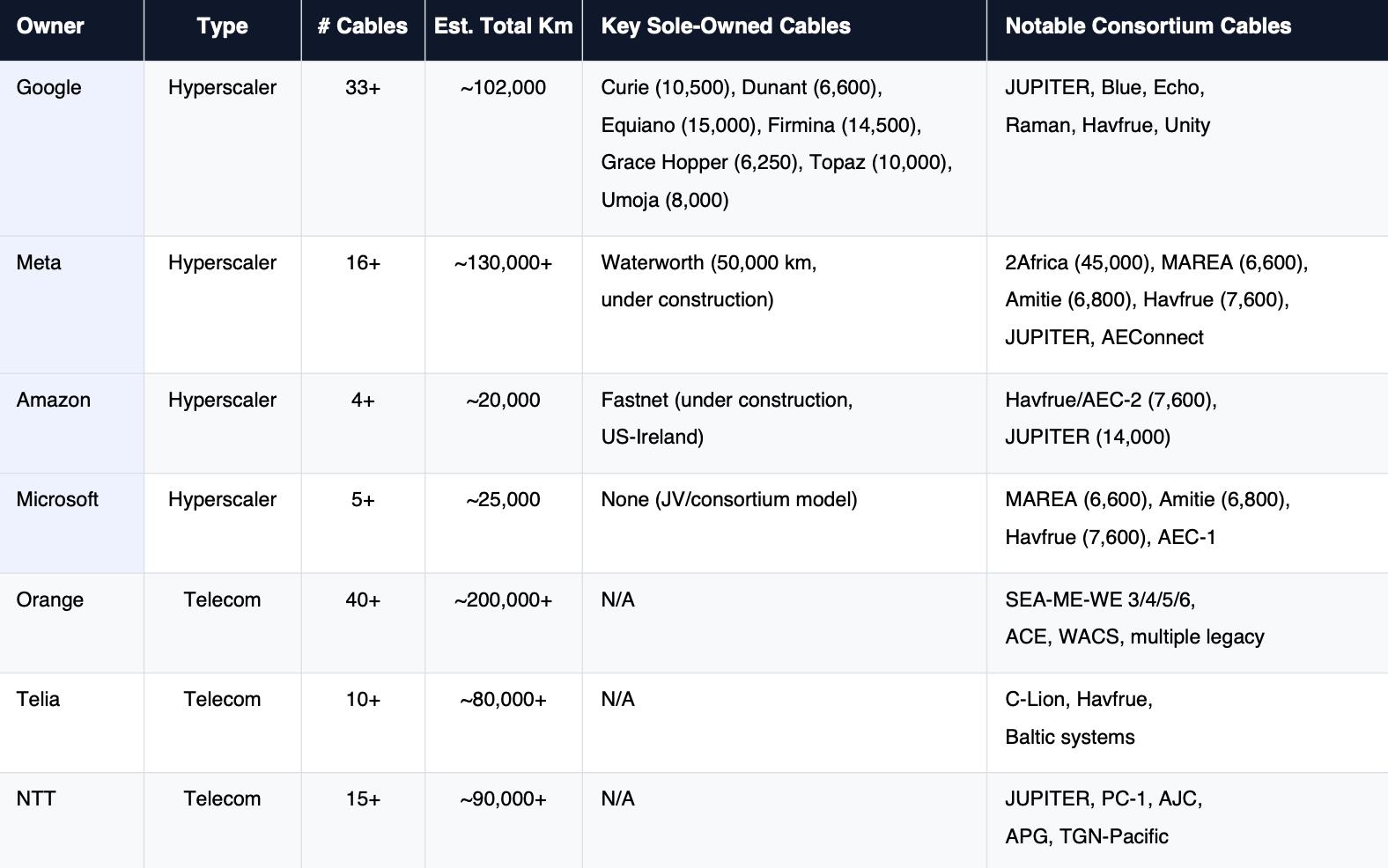

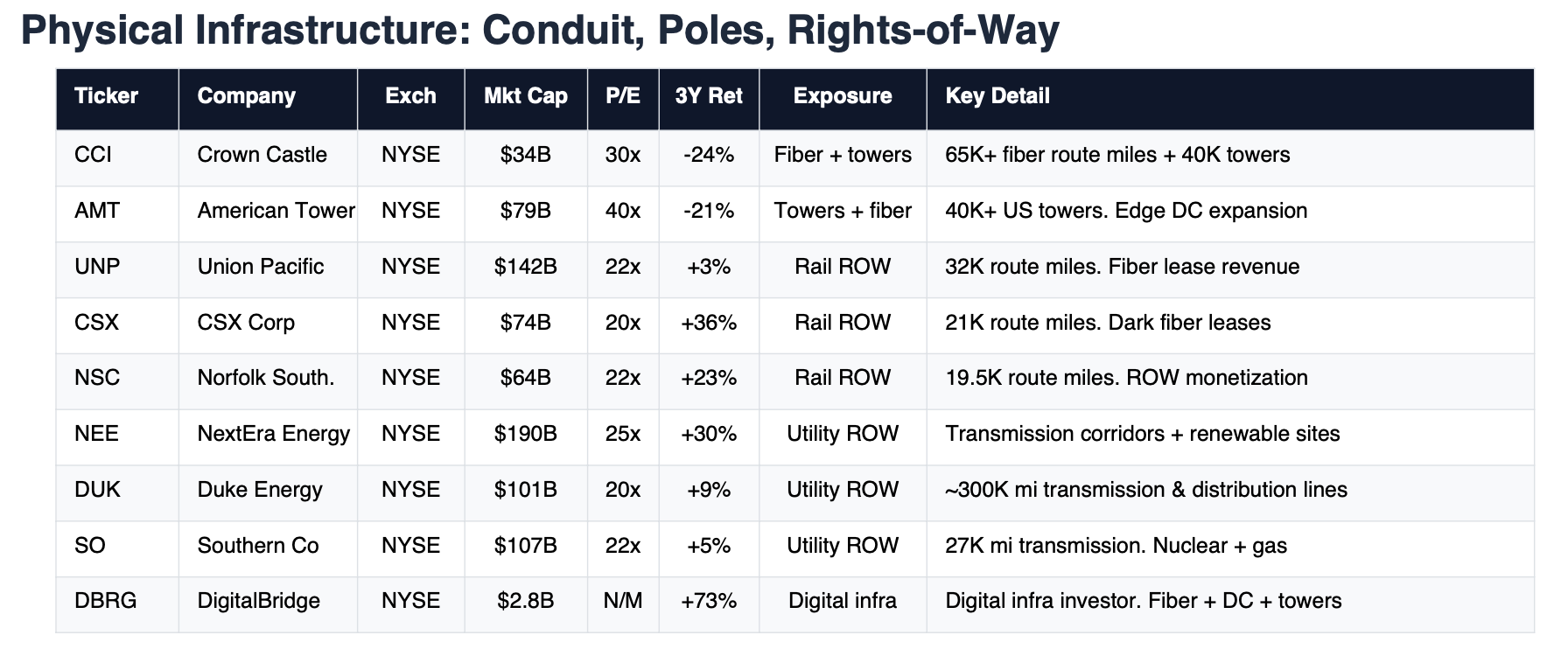

Large players such as Meta Platforms META 0.00%↑ and Google have already invested heavily in these networks, gaining not only cost advantages but also greater control over data flows and network reliability. This reduces dependence on third-party providers and strengthens their position across the broader digital ecosystem.

Hyperscalers are rapidly vertically integrating their network infrastructure, with Google, Meta, Microsoft and Amazon now owning or co-owning more than 40 subsea cables. This shift gives them greater control over global connectivity and reduces reliance on traditional consortium models.

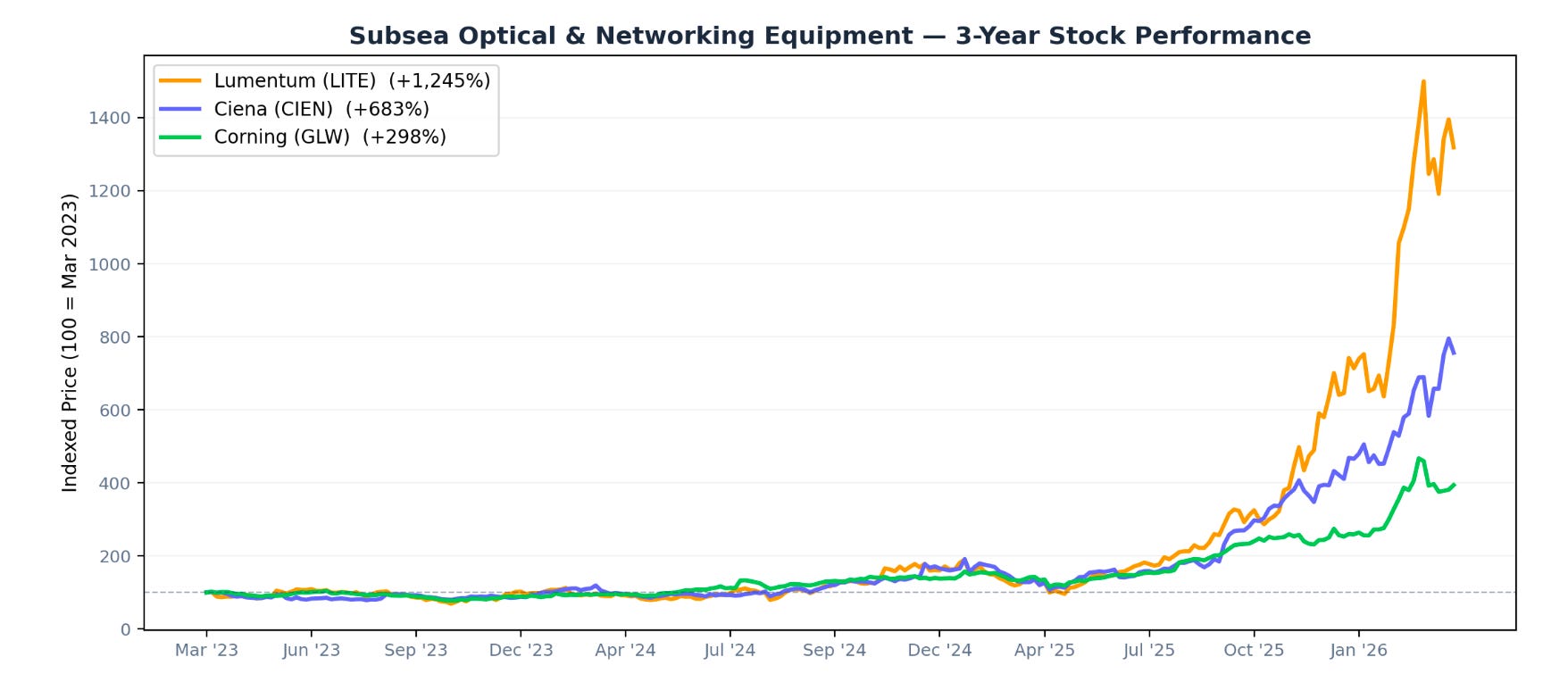

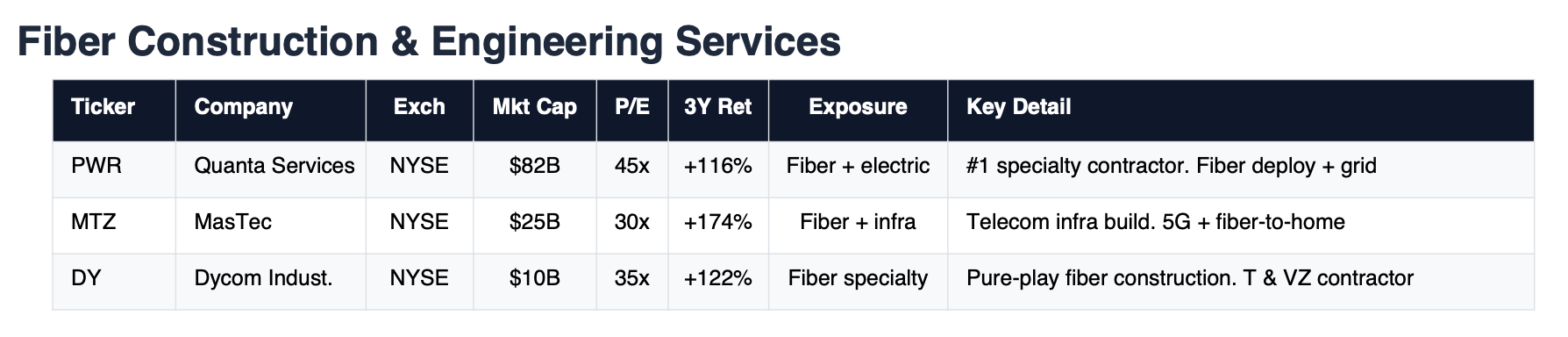

At the same time, equipment makers such as Ciena CIEN 0.00%↑, Lumentum LITE 0.00%↑ and Corning GLW 0.00%↑, along with Japanese fiber producers like Sumitomo and Furukawa, have seen strong growth driven by rising demand for subsea and datacenter interconnect.

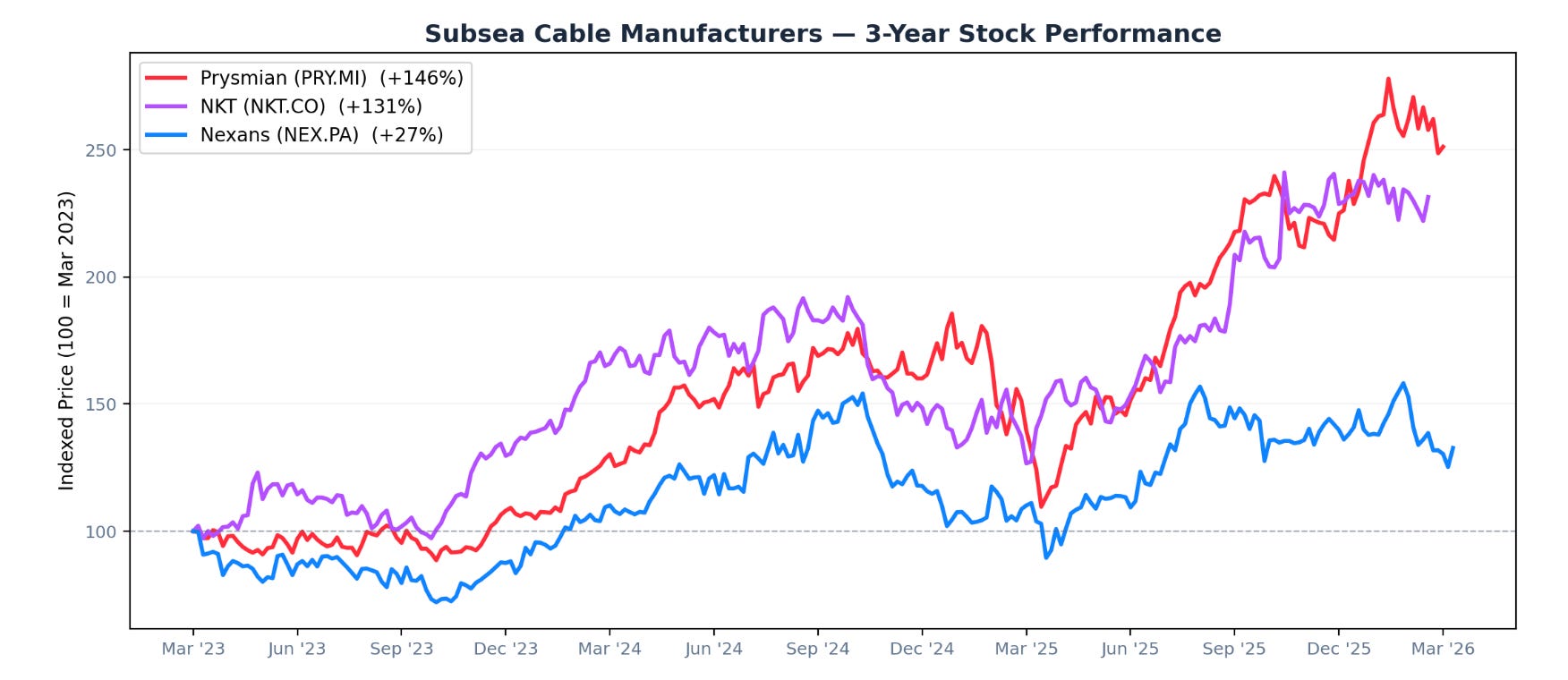

European manufacturers including Prysmian, Nexans and NKT still dominate subsea cable production, while Chinese players like Hengtong and ZTT are expanding quickly. Installation remains a key constraint due to limited cable-laying vessel capacity from companies such as Subsea 7 and Saipem, creating backlogs and pricing power. As AI workloads grow, both subsea and terrestrial fiber are becoming essential infrastructure for moving large volumes of data between distributed data centers.

The result is a reinforcing cycle similar to what has played out in semiconductor manufacturing. Companies that built early benefit from lower capital intensity, higher utilization, and stronger margins, which in turn fund continued investment into next-generation infrastructure. Meanwhile, rising input costs act as a barrier to entry, making it increasingly difficult for competitors to replicate this scale with comparable economics. In this environment, inflation does not just increase costs, it entrenches incumbents, effectively locking in their advantage over time.

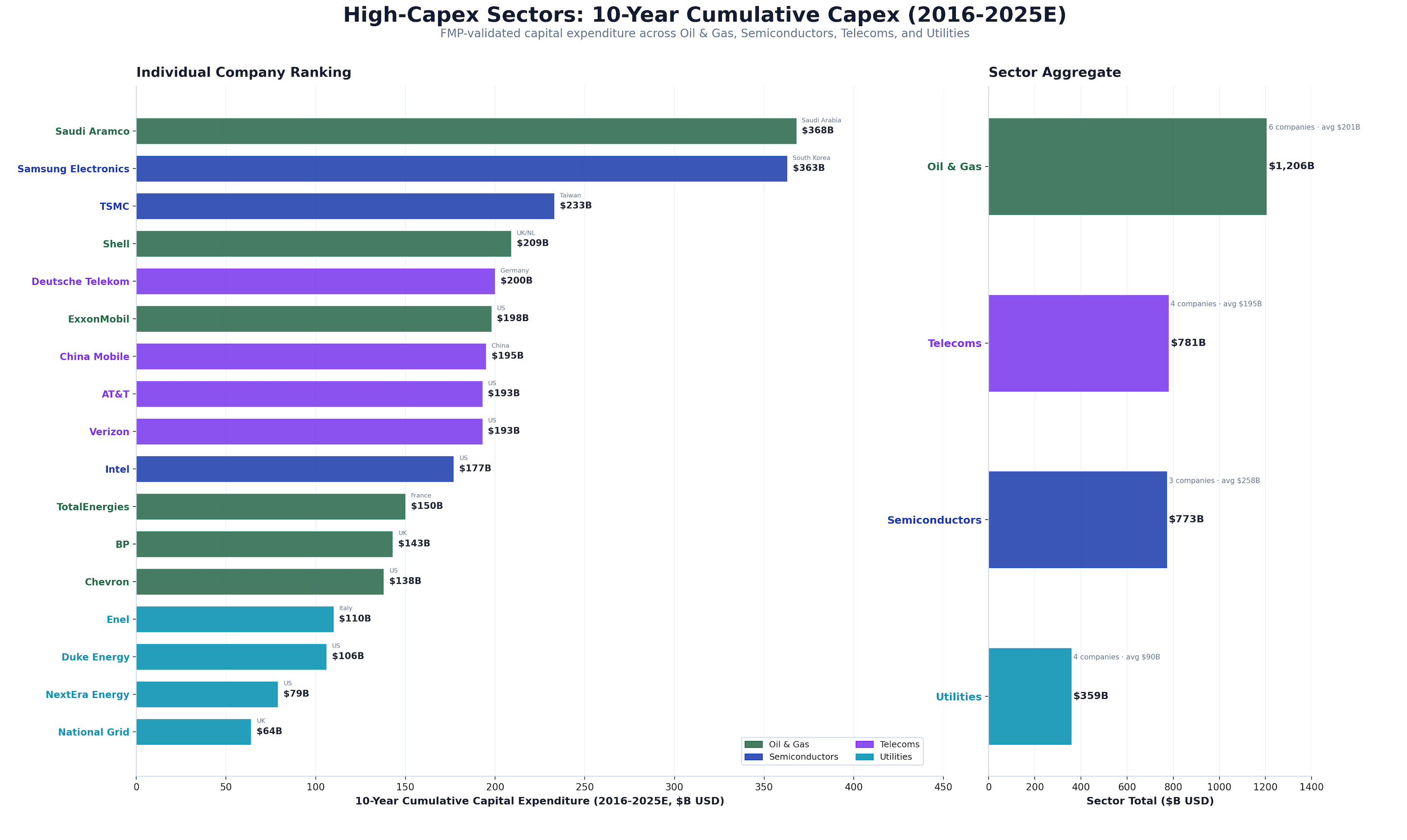

Other capital-intensive sectors of the economy include Oil & Gas, Telecommunications, Semiconductors and Utilities. Prominent companies in these industries include Saudi Aramco, Samsung, TSMC, Shell, Deutsche Telekom, among others.

I believe new infrastructure build-out will only accelerate once the unit economics are clearly attractive. In the oil sector, returns have historically lagged the rest of the market, with gains typically emerging during geopolitical conflicts. Policies like the EU’s 2022 “excess profits” tax further limit incentives for new investment, keeping build-out cautious.

Combine this with expectations of an economic slowdown, rising commodity prices, and the long lead times for infrastructure build-out, and there is little incentive to start adding new capacity based on current market conditions.

These factors suggest that the energy rally may be more persistent than commonly expected. While short-term volatility has drawn the most attention the prices on the long end are surpassing the previous highs, signalling a stickier market than most anticipate.

Among mega-cap tech companies, Apple stands out for its relatively low CapEx intensity, reflecting its strategy of focusing on hardware, software and ecosystem integration rather than building large-scale infrastructure. With its deep device penetration, Apple AAPL 0.00%↑ is well positioned to play a central role in AI distribution, even as rising component costs make significant market share shifts more difficult.

While some margin pressure is possible, it is not inevitable. Apple’s control over hardware and silicon could help offset cost increases, particularly as on-device inference becomes more important. This positions Apple as a key player in the unit economics of LLM distribution, both as a distribution layer and by enabling partial local inference that can reduce costs for model providers.

It is interesting to see how Apple, unlike other mega-cap techs, has taken a distinct approach to safeguarding its business against the uncertainties ahead.

To wrap up..

I continue to believe we are in the early stages of a new commodity cycle. Energy shocks in 2026, ongoing geopolitical conflicts and slowing economic activity increase the likelihood of a recession, while elevated debt levels, thin liquidity and stretched valuations raise the risk of a financial shock that could trigger monetary debasement.

At the same time, AI’s impact on the labor market could limit opportunities for many workers to stand out economically, likely increasing the demand for government support programs such as food stamps or universal basic income.

In this environment, well-capitalized, asset-heavy companies are positioned to benefit from or withstand left-tail shocks, leveraging structural demand, high barriers to entry and strong balance sheets in a challenging macroeconomic landscape.

The Mag-7 management seems aware of this, echoing the old Buffett principle regarding railroads: focus on businesses with durable competitive advantages, high barriers to entry and predictable cash flows.

Given the weight of the Mag-7 in major indexes, it may be more important for them to protect their moats through vertical integration, even while publicly framing it as a race to lead in AI. If defending their strategic positions is truly structurally important, then the high current market valuations were likely necessary to fund these initiatives.

Here are a few companies I may cover in a future article:

Excelente artigo, JP. A tua análise sobre o CapEx como o novo moat económico é cirúrgica. No entanto, acredito que o destino final desta infraestrutura vai muito além do software e da Cloud: é a fundação física para o 5G/6G, IoT e Indústria 4.0.

Mas há uma camada acima disto que torna este moat assustador: a Geopolítica. Este brutal aumento de custos não bloqueia apenas empresas concorrentes; bloqueia nações inteiras. Os EUA (Wall Street + Silicon Valley) parecem estar a usar a inflação de forma estratégica para encarecer a construção de infraestrutura à China e ao Sul Global, enquanto diluem a própria dívida e asseguram energia barata nas Américas.

Isto vai dividir o mundo em dois blocos tecnológicos, obrigando os restantes países a cederem soberania para não ficarem na idade das trevas da produtividade. Este teu artigo fez-me pensar tanto nisto que vou criar um Substack e escrever o meu primeiro texto a expandir exatamente esta tese macro/geopolítica. Parabéns pela newsletter e por puxares pela cabeça do pessoal!